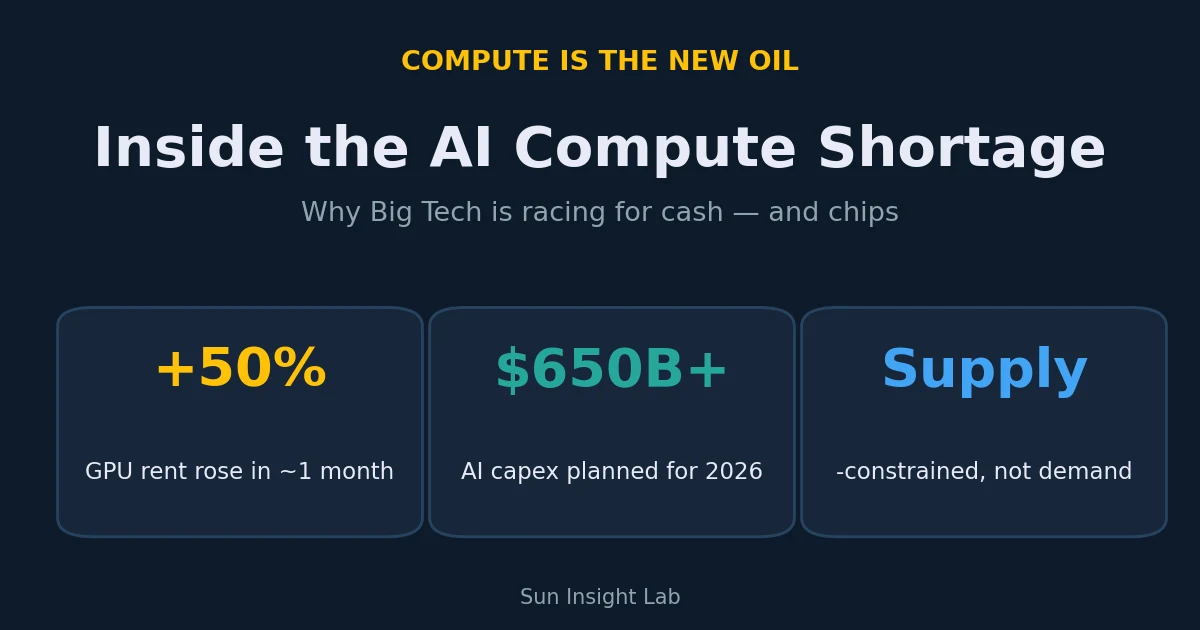

Google Paid 50% More for the Same AI Chips in 30 Days — Here's What the Compute Shortage Really Means

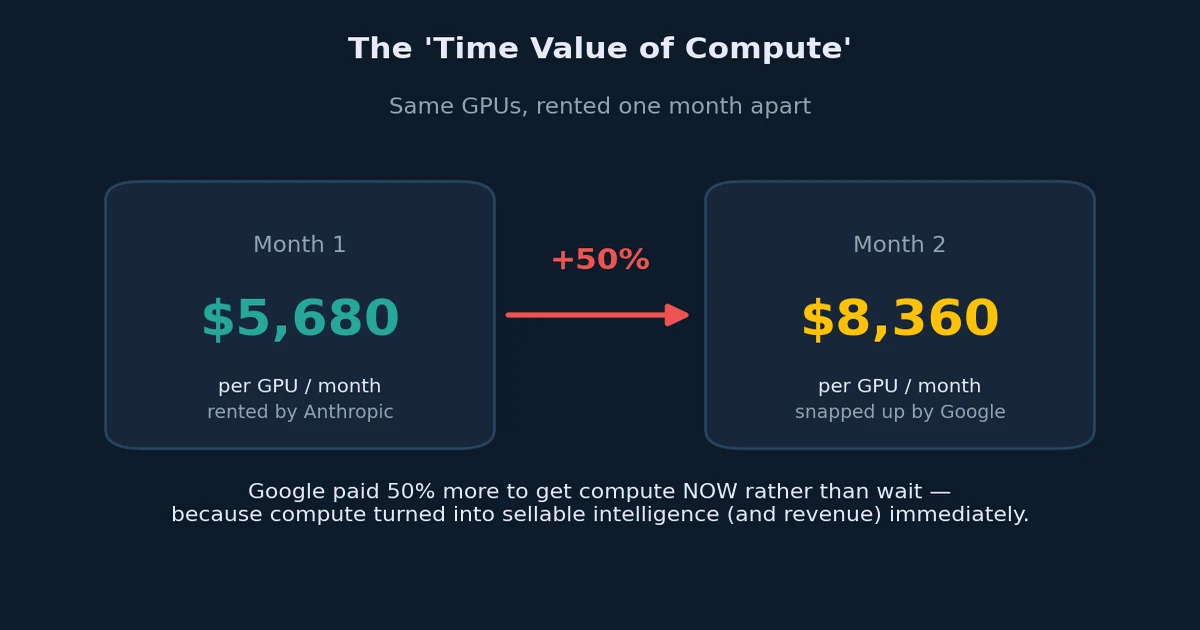

Here is a number that should stop you mid-scroll. One AI lab rented a batch of GPUs for about $5,680 per chip per month. Roughly thirty days later, when another buyer came for the same kind of capacity, the price had jumped to about $8,360 — and the buyer, Google, reportedly said thank you and took it anyway. A 50% price hike in a single month, paid willingly, for hardware that is otherwise sitting in a data center. To understand why one of the most cash-rich companies on Earth would do that, you have to understand the single idea now reshaping markets: compute has become the new oil.

Compute Is the New Oil

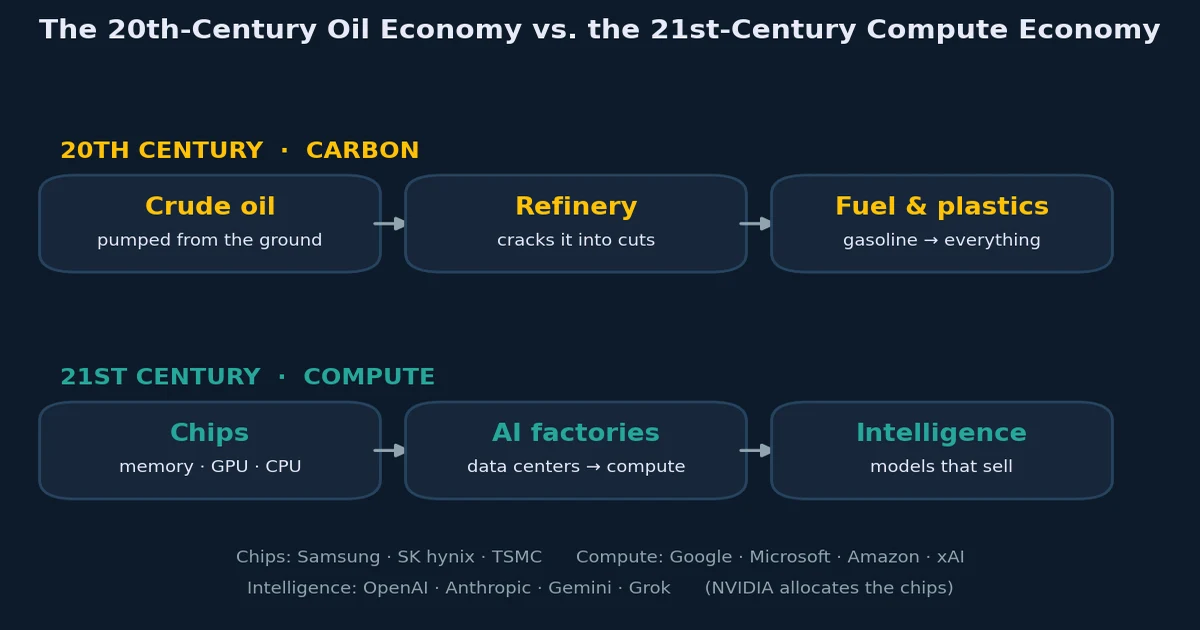

For most of the 20th century, the economy ran on crude. You pumped oil out of the ground, sent it to a refinery to be cracked into gasoline, diesel, jet fuel and asphalt, and then turned the leftover naphtha into the plastics and chemicals that touch nearly every product you own. Raw input, refined into something useful, sold into endless demand. That was the carbon economy.

The 21st-century version runs on the same shape, with different parts. The "crude oil" is now semiconductor chips — memory, CPUs and especially GPUs — produced by companies like Samsung, SK hynix and TSMC. Those chips flow into what you can think of as AI factories: the data centers run by Google, Microsoft, Amazon, xAI and a crop of specialized "neocloud" providers, where raw silicon is refined into compute. And compute, in turn, is fed to the model makers — OpenAI, Anthropic, Google's Gemini, xAI's Grok — who refine it into the final product: intelligence that can be sold.

One company sits in the middle as the gatekeeper: NVIDIA. Because it controls how scarce GPUs get allocated, it effectively decides who gets to build the most compute, the way a general contractor decides which sites get the steel first. That structure matters, because it means the whole chain is gated by supply — and right now, supply is the problem.

The "Time Value of Compute"

Back to Google paying 50% more. The reason isn't carelessness — it's arithmetic. Economists talk about the "time value of money": a dollar today is worth more than a dollar next year, because you can put today's dollar to work. The AI race has created the same logic for hardware — call it the time value of compute.

If you can take a GPU today and immediately turn its compute into intelligence that customers are lining up to buy, then waiting six months is enormously expensive — you forfeit six months of revenue. So the real question a buyer faces isn't "is this chip cheap?" It's "would I rather have compute now, or 50% more cash later?" When the product you can make sells as fast as you can make it, paying a steep premium to start today is the rational move. Google's willingness to eat a 50% increase is not a sign of a bubble mindset; it's a signal of how immediately compute converts into money right now.

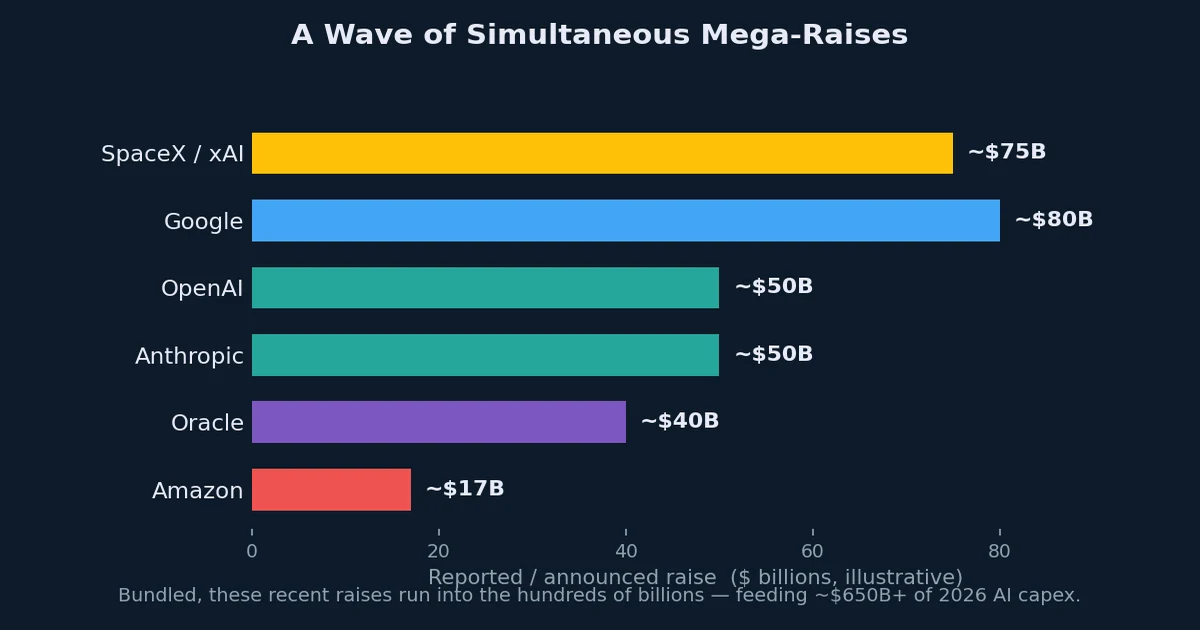

The Cash Scramble That Rattled the Market

That hunger has a side effect. If everyone wants compute now, everyone needs cash now — and over a short stretch the biggest names in tech lined up for capital almost simultaneously. Headline raises and reported plans piled up across SpaceX/xAI, Google, OpenAI, Anthropic, Oracle and Amazon, bundling into the hundreds of billions of dollars in a remarkably short window.

When that much money gets drawn out of the system at once, something has to give. Cash to fund these raises gets pulled from somewhere, and the easiest place to raise it is to sell what has already gone up. That dynamic — liquidity being vacuumed toward AI infrastructure — is a clean explanation for why broad equities wobbled even as the AI story stayed intact. The figures above are best read as illustrative of the scale rather than precise, confirmed totals, but the direction is unmistakable: this is the most capital-intensive buildout in living memory.

Is the Money Actually There?

The natural worry is whether the system can absorb a draw this large. Here the numbers are reassuring. Even a few hundred billion dollars of raises is small against a U.S. stock market worth roughly $69 trillion, and there is something like $8 trillion parked in money-market funds earning yield and looking for a home. The capital exists. What decides whether it flows is a single judgment: do lenders and investors believe this money will come back with a return? Given that the buildout is already booked — independent analysts peg 2026 AI infrastructure spending from the largest players at well above $650 billion, with the market described as supply-constrained rather than demand-constrained — the bet is that compute keeps converting into revenue faster than it can be built.

It's worth noting how the bottleneck is shifting, too. The earliest squeeze was raw GPUs. Increasingly the binding constraint is mundane physical infrastructure — electrical transformers, switchgear and grid connections — where lead times have stretched to multiple years. The shortage is real; it's just migrating down the stack from chips to the power that energizes them.

Key Takeaways

The cleanest way to hold all of this in your head is the oil analogy: chips are the crude, data centers are the refineries, and intelligence is the product — with NVIDIA controlling the taps. The reason valuations and capital spending look extreme is the time value of compute: when a unit of compute turns into sellable intelligence almost instantly, buyers will pay sharp premiums to get it sooner, and builders will raise enormous sums to supply it. That simultaneous scramble for cash is the most plausible reason the broader market hiccuped recently, even though nothing about the underlying demand broke. For an investor, the practical lesson isn't to chase every AI headline or to flee every dip — it's to keep your eye on the durable mechanics (who supplies compute, who controls allocation, where the next bottleneck forms) and stay disciplined through what is going to remain a very volatile build-out.

This article is for educational purposes only and does not constitute investment advice. Specific funding figures and rental prices cited here are illustrative of the scale and dynamics discussed and may differ from confirmed company disclosures; verify independently before relying on them. AI-related stocks can be highly volatile.

Back to Analysis | Return to the Quant Lab | Open the Simulator