Circle Isn't a Crypto Company — It's a Treasury Bill Fund. Here's Why That's About to Change.

Circle — the company behind USDC, the world's second-largest stablecoin by market capitalization — has become one of the more talked-about names in digital finance. Its stock moved dramatically in early 2026: up roughly 130% over three weeks as the U.S. CLARITY Act gained momentum, then down about 36% in the following 16 days as the bill stalled and a specific provision triggered concern. To understand those swings, you first need to understand what Circle actually does and where its money comes from. The answer is simpler — and more concentrated — than most people expect.

What USDC Is and How It Works

A stablecoin is a digital token designed to hold a fixed value relative to a real-world currency — in USDC's case, one token equals one U.S. dollar at all times. The mechanism is straightforward: a user deposits dollars with Circle, and Circle issues an equivalent amount of USDC tokens in return. Those tokens can then be used across cryptocurrency exchanges, decentralized finance platforms, payment networks, and increasingly, corporate treasury operations. When the user wants their dollars back, they return the tokens and Circle redeems them at par.

Think of it like a digital receipts system. Your dollars go in, a digital receipt (USDC) comes out, and the receipt is usable anywhere that accepts it — globally, instantly, and at any hour. When you no longer need the receipt, you hand it back and receive your dollars. The stablecoin itself does not pay interest to the holder. That detail is the key to understanding Circle's business.

The Business Model: Earning Interest You Do Not Pass On

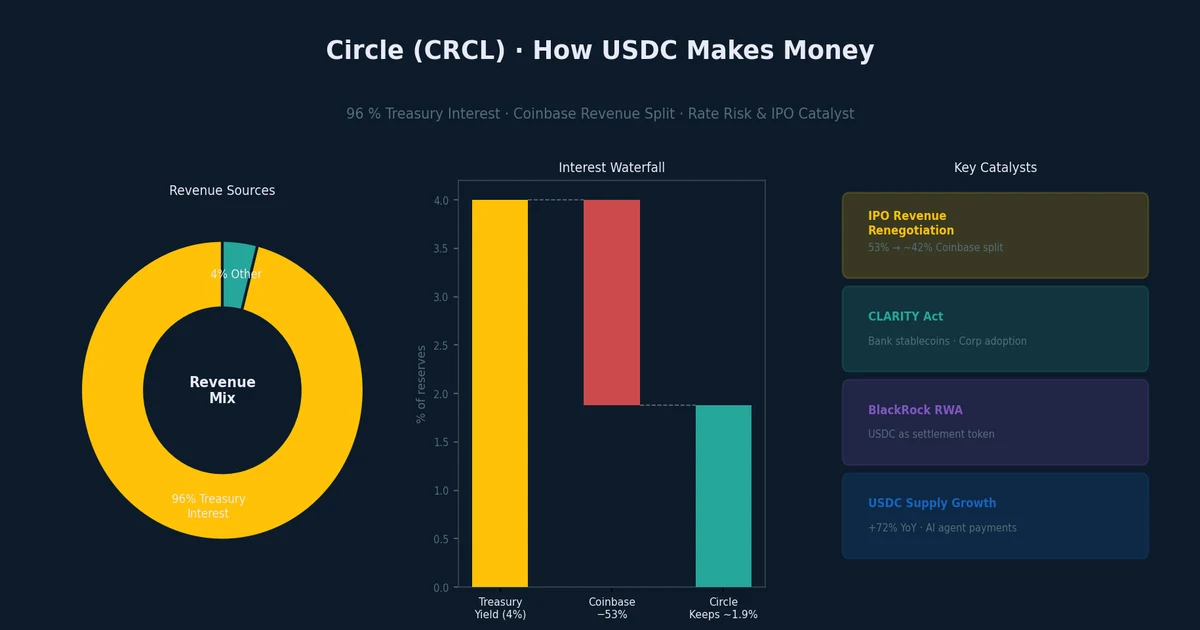

While USDC holders receive no interest, Circle does not simply hold the deposited dollars in a vault. It invests those reserves in short-term U.S. government securities — primarily Treasury bills and money-market funds — and keeps the yield for itself. At current rates, that return is roughly 4% annually on the full reserve pool. Since the company does not pay any of that yield to USDC holders, the spread between what Circle earns on reserves and what it pays depositors (zero) is its primary revenue stream.

This structure differs from a commercial bank in one important way. Banks operate on a fractional reserve system: they hold perhaps 7–10% of deposits in reserve and lend the rest out to earn interest on loans. If too many depositors withdraw at once, a bank can face a liquidity crisis. Circle, by design, cannot do this. Regulations require it to hold dollar-for-dollar backing for every USDC in existence, and that backing must sit in the safest assets available — short-term Treasuries and government money-market funds. No lending, no leverage. This makes Circle considerably safer than a bank for depositors, but it also means the only knob Circle can turn to increase revenue is the size of the USDC supply and the prevailing interest rate on short-term government debt.

The revenue concentration is striking. Approximately 96% of Circle's total revenue comes from Treasury interest. The remaining 4% — labeled "other revenue" in its financials — has grown rapidly (reportedly around 15x year over year by early 2026) through fees from its own payment network, business-to-business services, and the ARCH settlement platform. But the core business is, as analysts have bluntly put it, an interest-rate business.

The Coinbase Problem — and Opportunity

USDC did not build its distribution network alone. For years, Coinbase — the largest U.S. cryptocurrency exchange — was essential to Circle's growth. Coinbase listed USDC prominently, made it the default trading pair on its platform, and drove enormous volume. In exchange, Circle agreed to share a large slice of its revenue. Historically, that share ran to approximately 53% of net interest income — meaning that for every dollar Circle earned on its reserves, it kept about 47 cents and paid Coinbase about 53 cents.

To visualize how that math works in practice: if the Treasury yield is 4% and Circle pays away 53% of that to Coinbase, Circle's effective yield on assets is roughly 1.9%. On a reserve pool of tens of billions of dollars, that is still a significant business — but the revenue share is why Circle's reported profit can look underwhelming relative to the headline size of the USDC market.

The situation is changing. Circle's IPO on Nasdaq — expected in mid-2026 — triggers a renegotiation of the Coinbase revenue-sharing arrangement. As Circle has grown from a startup entirely dependent on Coinbase's distribution into an independently listed company with its own payment network, Visa partnership, and BlackRock collaboration, its negotiating position has improved considerably. Analysts covering the stock estimate the revenue share could fall to the 40–45% range from the current 53%. That shift, if it materializes, would directly add several hundred million dollars to Circle's operating income with no corresponding increase in costs — a pure margin expansion event.

The CLARITY Act: Bad Headline, Potentially Good Outcome

The U.S. CLARITY Act is proposed federal legislation that would establish a regulatory framework for stablecoins. One of its provisions — the one that triggered Circle's sharp stock decline in early 2026 — would prohibit exchanges like Coinbase from paying interest on stablecoins held in customer accounts.

At first glance this sounds like bad news for the entire stablecoin ecosystem. But consider the second-order effect: if Coinbase can no longer offer yield on USDC holdings, one of its key bargaining chips in negotiating revenue share disappears. Coinbase currently argues that its platform creates value by making USDC attractive to users through yield programs. Remove that, and Circle gains leverage. The same regulation that caused a short-term sell-off in Circle's stock may structurally improve the terms of its most important business relationship over the longer run.

The CLARITY Act also contains provisions that, if passed in full, would allow banks to issue stablecoins and permit corporations to use stablecoins in accounting ledgers as recognized financial instruments. Both expansions would dramatically increase the addressable market for USDC and open institutional distribution channels that currently have no formal regulatory footing.

How USDC Is Actually Being Used

It is easy to assume that stablecoins are primarily a tool for cryptocurrency speculators moving between positions. That is still a major use case, but USDC's growth in 2025–2026 has come from several additional sources.

Digital collateral in decentralized finance. A significant share of USDC circulation comes from crypto holders who want liquidity without selling appreciated positions. An early Bitcoin buyer with a low cost basis — say, a purchase price of $30,000 or $40,000 per coin — may be reluctant to sell at much higher prices and trigger a taxable event. Instead, they post their Bitcoin as collateral against a loan denominated in USDC, deploy that USDC to buy more assets, and effectively use their existing holdings to access capital. USDC is preferred for this because its value does not fluctuate, making collateral calculations stable.

Cross-border payments. Sending money internationally through the SWIFT banking network typically costs $30–40 in fees and takes one to several business days to settle. Sending USDC costs under $1 in transaction fees and settles in minutes, regardless of geography. This advantage has made USDC increasingly attractive to businesses with international supply chains, remittance providers, and individuals sending money across borders. Visa has formally integrated USDC as a settlement asset within its payment network, adding a layer of institutional credibility and mainstream accessibility.

Treasury management by crypto projects. Blockchain projects that have raised capital by issuing their own tokens typically hold those treasury funds in some combination of Bitcoin and stablecoins. When market conditions look uncertain, they often rotate treasury holdings from Bitcoin into USDC to protect purchasing power. This "store-of-value" use case drives a significant portion of USDC's float — tokens that sit largely idle but still count as circulating supply on which Circle earns interest.

AI agent micropayments. This is the newest and most speculative use case, but the one generating the most forward-looking discussion. As AI agents become capable of executing financial transactions autonomously — trading, paying for data, compensating other agents for services — they need a payment rail that is programmable, instant, borderless, and cheap. Traditional financial rails are too slow, too expensive, and too dependent on human authorization processes for the kind of high-frequency, low-value transactions AI-to-AI commerce would require. USDC, operating on smart-contract infrastructure, is technically well-suited for this. Currently, AI agent transactions account for an estimated 1–2% of USDC volume — small but growing, and a category that did not exist at scale even two years ago.

Where USDC Circulation Is Going

USDC's overall circulation grew approximately 72% year over year through early 2026. Transaction volume grew even faster, up roughly 96% — meaning not only are more tokens outstanding, but each token is being used more actively. Within that growth, the distribution of where USDC circulates is shifting. External platforms (primarily Coinbase and other exchanges) accounted for 75% of USDC usage a year ago; that figure has dropped to around 59%. Circle's own platforms and direct integrations have grown from 5% to 17% of total usage. This shift matters for profitability: revenue generated through Circle's own channels does not carry the 53% revenue-sharing cost that exchange-routed volume does.

BlackRock's Real World Asset (RWA) tokenization program has formally designated USDC as its settlement token of choice. RWA tokenization — putting real financial assets like government bonds, real estate debt, and private credit onto blockchain rails — is a nascent but rapidly expanding area. BlackRock's endorsement effectively means that as institutional-grade tokenized assets grow in volume, the plumbing underneath them runs on USDC.

The Interest Rate Risk

The single largest risk to Circle's financial model is the direction of U.S. interest rates. With 96% of revenue tied to the yield on short-term Treasuries, a sustained Fed rate-cutting cycle directly compresses Circle's revenue on the same asset base. The Federal Reserve cut rates several times in 2024 and early 2025, and Circle's margins moved with them. This is not a subtle relationship — it is essentially the entire business.

The partial offset is that lower rates tend to encourage more risk-taking in financial markets, which historically increases crypto trading volumes and therefore USDC circulation. More USDC in circulation partially compensates for lower yield per token. But the math only works above a certain rate floor, and at very low rates the interest income would shrink faster than circulation could realistically grow.

Competition is the secondary risk. Tether (USDT), the largest stablecoin, is attempting to enter the U.S.-regulated market, though it would first need to restructure its reserves to comply with U.S. requirements — a non-trivial undertaking. JPMorgan's JPM Coin operates as an institutional deposit token within JPMorgan's own ecosystem and is not a direct competitor for retail or crypto-native use cases. European regulations (MiCA) are actively restricting Tether's operations there, which has opened market share for USDC in European crypto markets.

The Catalysts Ahead

Several specific events could move Circle's financial picture materially in the next 12–24 months. The IPO revenue-share renegotiation with Coinbase is the most immediate — it is a contractual reset that happens at a defined moment and has a quantifiable impact on margins. The CLARITY Act's passage (or continued stalling) will define how quickly banks can issue competing stablecoins and whether corporate adoption gets regulatory clarity. BlackRock's RWA volume growth is a slower, more structural tailwind. And Circle has announced CirBTC, a Bitcoin-backed token — an attempt to bring the stablecoin model to the Bitcoin ecosystem and access DeFi collateral use cases that currently favor Ethereum-based assets.

None of these catalysts is guaranteed to arrive on schedule. Legislation moves unpredictably. Revenue renegotiations can disappoint. New products take longer to gain traction than projected. These are the standard risks of investing in a company at the intersection of financial regulation and emerging technology. But the underlying business — issuing the digital dollar infrastructure for a world that is slowly moving more commerce onto blockchain rails — has a clearer long-term logic than most crypto-adjacent companies that have listed in recent years.

Key Takeaways

Circle's revenue comes almost entirely from the interest it earns by investing USDC reserves in U.S. Treasuries — a structure that is simple, transparent, and directly tied to Federal Reserve policy. The company pays nothing to USDC holders, keeps the yield, and shares a large portion of that yield (historically 53%) with Coinbase. An IPO-triggered renegotiation of that split is the single most tangible near-term profit catalyst. USDC circulation and transaction volume are growing strongly, with diversification away from exchange dependence. Use cases are expanding from crypto trading into cross-border payments, DeFi collateral, institutional settlement, and early AI agent commerce. The primary risks are interest rate direction, regulatory timing, and competition from Tether and bank-issued alternatives. The CLARITY Act — despite triggering a sharp short-term sell-off — may prove structurally beneficial for Circle by reducing Coinbase's negotiating leverage and opening institutional distribution channels.

This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Circle (CRCL) is a publicly listed company and all investment decisions carry risk.